As we approach 2025, the Financial Services industry is navigating a dynamic interplay of economic challenges, regulatory implementations and technological innovations that are reshaping industry priorities and highlighting the urgent need to modernize legacy infrastructure. These trends are impacting customer experience and profitability. According to Forrester, the customer experience index for banks has declined globally for three consecutive years.

The exploration of the economic landscape and emerging trends in data, AI, customer experience and regulatory compliance is necessary for financial institutions to adapt to the demands of the future.

Balancing market events: aggressive cuts and defensive measures

The industry remains focused on central banks’ monetary policies to achieve a "soft landing" by controlling inflation without triggering a recession. Incremental interest rate cuts by the Federal Reserve have slowed inflation, but financial institutions remain cautious about risks to consumer and corporate lending. Despite recent challenges, 2024’s Q3 earnings for major banks, such as JPMorgan, have exceeded expectations, signaling hope for a soft landing. However, continued interest rate cuts in 2025 could challenge revenue streams in consumer, commercial and mortgage lending sectors that are highly sensitive to rate fluctuations.

Simultaneously, regulatory shifts are reshaping financial landscapes. Section 1033 of the Dodd-Frank Act, finalized in October 2024, enhances consumer data rights, fostering innovation in open banking and lending. The global implementation of ISO 20022, mandatory by March 2025, standardizes financial messaging formats, transforming cross-border transactions with greater accuracy and efficiency.

In response, financial institutions are intensifying investments in technology to enhance compliance, streamline operations and elevate customer satisfaction. Open banking, embraced globally, enables consumers to securely share their banking data with third-party providers, driving competition and innovation. Leveraging real-time data under Section 1033 enables personalized lending, while ISO 20022 enhances transaction transparency and risk assessment, helping banks adapt to dynamic market conditions.

As regulatory and technological shifts are implemented, financial institutions must address these critical challenges.

Accelerating data and AI charters is a foundational cornerstone of technology that empowers financial institutions to overcome these challenges and thrive in a dynamic environment.

Leveraging data and AI for transformation

The introduction of Section 1033 demands secure and accurate data sharing with third-party providers. AI-driven tools enhance confidence in open banking data through real-time validation, anomaly detection and fraud prevention. These capabilities not only ensure regulatory compliance but also help financial institutions deliver personalized and innovative customer experiences.

While legacy systems are foundational, this often hinders banks from achieving the agility and efficiency demanded by current markets. AI tools can analyze and break down old, monolithic applications into smaller independent microservices. Utilizing AI will allow financial institutions to evolve. Prioritizing API-driven architecture will allow an easy connection between legacy systems with AI and other modern applications. Additionally, AI-driven insights from legacy systems can help financial institutions identify inefficiencies, prioritize upgrades and reduce operating costs, enabling a smoother transition to future-ready platforms.

Good data enables better AI governance by ensuring data quality, accuracy and reliability. Implementing a strong data governance framework is crucial for mitigating enterprise risks. AI-ready data is available, complete, accurate and high quality. AI governance practices include sound AI policy, regulation and data governance.

AI will enable financial institutions to incorporate data beyond traditional data sources, unlocking more value with alternate and external datasets. By parsing nontraditional data- such as social media, geospatial data and real-time economic indicators- AI systems can improve upon decision making processes across various domains. Processes including credit scoring, risk assessment and fraud detection can utilize this data providing a clearer and more personalized offering for consumers. This capability is highly impactful in underserved markets or consumers with limited credit histories where traditional data may be insufficient.

The financial services landscape in 2025 will be defined by its ability to adapt to economic fluctuations, embrace new regulatory standards and leverage advanced technology. By modernizing legacy systems, harnessing data and AI, implementing robust data strategies and transforming infrastructure, financial institutions can navigate the complexities of a rapidly evolving market.

HCLTech: Driving innovation in financial services

HCLTech stands at the forefront of these transformations, offering tailored solutions to assist financial institutions overcome challenges and seize opportunities. HCLTech AI labs provide a comprehensive framework for embedding GenAI capabilities to enhance critical banking processes such as KYC (Know Your Customer) and trade surveillance for compliance. By leveraging real-time data insights, the power of AI ensures that customer verification is accurate, efficient and compliant with stringent regulatory standards.

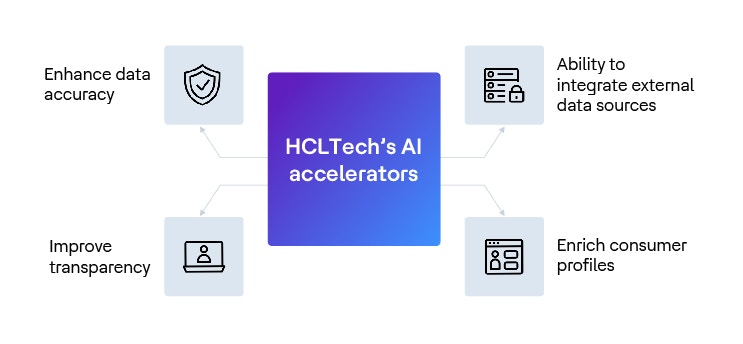

HCLTech’s AI accelerators are designed specifically for financial institutions, enabling fraud detection, predictive analytics for credit risk and personalized customer experiences.

As a trusted partner, HCLTech combines deep domain expertise with innovative technologies, empowering financial institutions to thrive in an ever-changing economic and regulatory environment.

References:

Predictions 2025: Banking | Forrester